Table of Contents

Everyone holding, trading, or investing in Bitcoin has the following questions on their minds. Is cryptocurrency legal? Should I pay taxes? Is there a way to pay less?

If we look at the map of Bitcoin legibility, we see that cryptocurrencies are legal in the EU and UK. But what does that mean? The main issue here is – how different governments view Bitcoin. Once that question is answered, the legality, and especially the taxation status is much more clear. This issue – whether a government is treating cryptocurrency as currency or asset, will determine the way it is taxed, if at all.

Is Bitcoin legal in the EU and UK?

Although in the last few years there was a flurry of legislative activity regarding cryptocurrencies, the national and the EU laws are not always clear on particular details covering all the possible use cases for Bitcoin and other e-coins.

What all the countries agree is that it’s not illegal, prohibited, or restricted to mine, own, or trade Bitcoin. What all the central, national, banks agree is that Bitcoin and other cryptocurrencies are volatile and risky investments.

From here, levels of government intervention differ from country to country. Ireland, Belgium, Malta, and a number of other governments declared that they will not regulate Bitcoins. Germany treats Bitcoin as a private asset. The UK sees cryptocurrency as property (a capital asset). Then there is Slovenia which declares Bitcoin neither a currency nor an asset, a stance ever since adopted by many others.

So, the definite answer is: YES!

Bitcoin is legal in the EU and UK. Legal to own, legal to mine, legal to be staked, used in liquidity pools, trade, exchange, etc.

It’s not a legal tender, though. El Salvador is currently the only country in the world that uses Bitcoin as its national currency. Just because something isn’t legal tender doesn’t mean it cannot be used for payment – it just means that there are no protections for either the customer or the merchant and that its use as payment is completely discretionary.

Using Bitcoin in EU and UK

So it is legal to own bitcoin. Let’s cover a few specific use cases, mining, trading, and participating in decentralized finances (DeFi) activities.

Mining

Crypto coins take their name after the complex cryptographic calculations needed for them to ‘materialize’. This process of creating (minting) new coins is called crypto-mining or simply – mining. The profitability of mining primarily depends on the prices of electricity, since running computers for extended periods of time is energy-consuming.

While mining is not illegal in the EU and UK, it is a practice that will see stricter regulation in the future, over ecology concerns as well as overall energy expenditure concerns. Most of the EU countries, however, recognize Bitcoin mining as – income. This is the way most countries will treat Bitcoins originating from the crypto mining process for taxation purposes.

Trading

Crypto trading is a very much misunderstood area when it comes to the legislature. This is where the EU regulations are unclear, where they differ from country member to country member. The confusion comes from the way cryptocurrencies operate. They can, indeed, be viewed as currency, as well as assets and financial instruments, depending on the way they are used. The government reactions will not always match the real use cases.

Because Bitcoin is legal in the EU and UK, owners can trade it, or exchange it for currency or other tokens. However, this exchange is not treated by the legal system as currency exchange, but as – trade.

Let’s say you have $100 and you want to change it to EUR. A licensed exchange office will make the exchange for you, using their exchange rate. You are not expected to pay any taxes. If you do the same exchange with fiat currency (USD, GBP, EUR) and Bitcoin, that transaction is VAT-free. But you might be subject to capital gain tax.

Once you trade Bitcoin for another cryptocurrency, for example, Ethereum, the legality of this case changes. Suddenly you are not trading in currency but in assets. Most legal systems in the EU and UK will treat this as a taxable event. Not for the purpose of VAT, but for the purpose of CGT (capital gain tax).

DeFi activities

Decentralized finances are quite a blind spot for many legal systems. Staking and liquidity pools really represent a gray area in terms of tax laws. Once you hold Bitcoin or any other currency token, it is legal to stake it or lend it to other users. How the taxation authorities see the gains and profits, is not always clear.

Staking is a practice of declaring or ‘locking’ a token you own to be ‘staked’ as proof that a blockchain network you support is credible. For example, the DOT token, the official currency of the Polkadot network can be staked to reinforce the credibility of the network, earning you rewards in DOT tokens.

While the staking itself is not a taxable event – it is simply declaring your tokens staked or transferring them to another wallet, the income from rewards is treated as gain. The EU and UK legislature are not 100% clear on how they treat income from staking rewards, but considering that they are very close to interest income, that’s how it would be treated. Even the USA’s IRS has no definite guide for staking rewards taxation.

Liquidity mining and yield farming are two similar practices in decentralized finances (DeFi). Basically, it is the practice of locking in or adding crypto assets to blockchain protocols and liquidity pools for earning passive income. Both practices will provide investors with rewards that are currently summarily viewed by tax regulators as interest income.

Because there is low interoperability between the networks, this might cause additional disputes. For example, you want to use your Bitcoin for liquidity mining on an Ethereum-based network. You will deposit your Bitcoin in escrow in exchange for an Ethereum-accepted token. This shouldn’t be a taxable event, because you are not selling your Bitcoin. However, watch out for legislative officers arguing that crypto-to-crypto trades are taxable, including this one!

Bitcoin and taxes

When it comes to taxes, legislative authorities of many countries are trying to apply the existing analogues from finances to Bitcoin. Tax comes in many shapes and forms, but we can talk about three major tax approaches:

- VAT – Value Added Tax, a percentage of the price, that applies to all commercial activities involving the production and distribution of goods, and the provision of services. Bitcoins are exempt from VAT, be it trading or mining.

- Income tax – This is the basic tax that government collects from income generated by individuals. It is often accompanied by national insurance (e.g. in the UK) as the main duty to be paid to the taxation authority.

- CGT – Capital Gain Tax, is a levy on the profit from an investment when the investment is sold. This usually applies to long-term gains, e.g. profit from assets held for more than a year. Capital gain tax is what most tax authorities will connect to your Bitcoin profits.

VAT

Value Added Tax is present at commercial activities. VAT is designed to be levied from the end-user or final consumer of a product or a service. As such, owning, holding, or interacting with Bitcoin and other cryptocurrencies doesn’t incur VAT tax on their value alone. Although there is no unified view of Bitcoin – many governments are hesitant to identify them as either electronic money, currency, negotiable instrument, security, voucher, or a digital product – they aren’t willing to declare it isn’t any of the aforementioned. However, it is accepted in the EU and UK that there will be no VAT on Bitcoin transactions.

If the merchant allows payment of goods and services in Bitcoin, and if the goods or services are subject to VAT, the transaction will be treated as if the goods and services were acquired by traditional currency. So, a customer will pay VAT, calculated in the price of the goods or services.

When it comes to services concerning the arrangement of transactions in Bitcoin, tax authorities see it in the same light as they see SWIFT services for traditional currency. In other words, if you have a digital wallet free of charge, no VAT is required. But if your digital wallet provider charges fees for the provision of their services, that is subject to VAT.

The same goes for exchange platforms. If your exchange platform charges a fee to use the platform, it will be subject to VAT, otherwise, no tax will be required.

Income Tax

Governments are vehemently trying to deny the ‘currency’ function of the cryptocurrency. Bitcoin is treated as an asset (or ‘property’ as USA’s IRS states). However, profits from Bitcoin trading are treated according to a ‘realization event’.

In other words, the government is very much interested to know how the profits from Bitcoin came to be. Long-term investments and gains from cryptocurrency held for over a year are counted as capital gains, while profits from trading or selling the crypto-assets held under a year are treated as short-term gains. These are taxed as income tax.

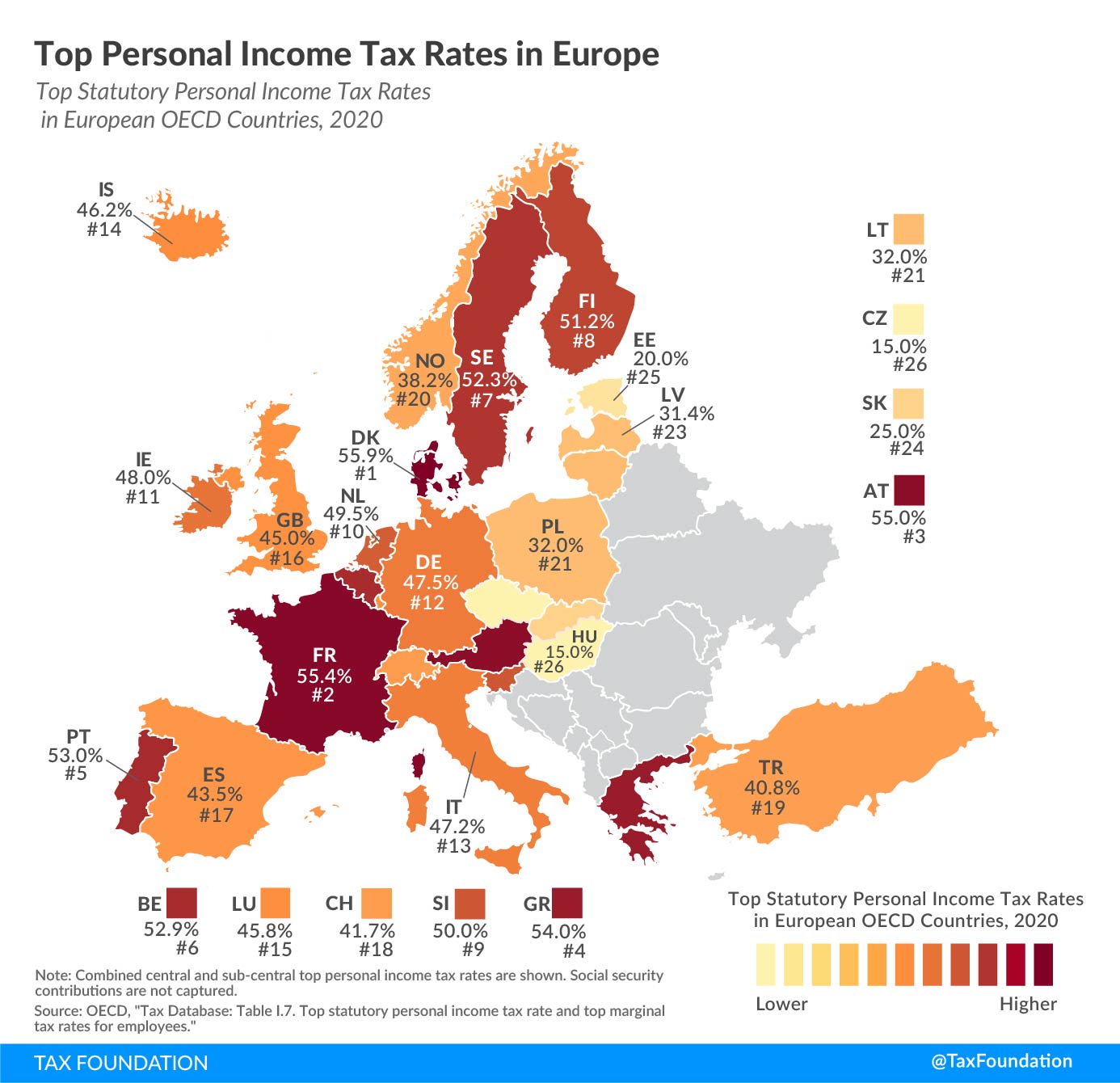

Income tax rates differ from country to country. Certain amounts are exempt from taxations. Tax rates vary not only by total income bracket but also by the status of a taxpayer (Single, married, head of household, etc). In Germany, for example, profits under 600 EUR are not taxed. In the UK, profits from crypto-trading are taxable over 1000 GBP.

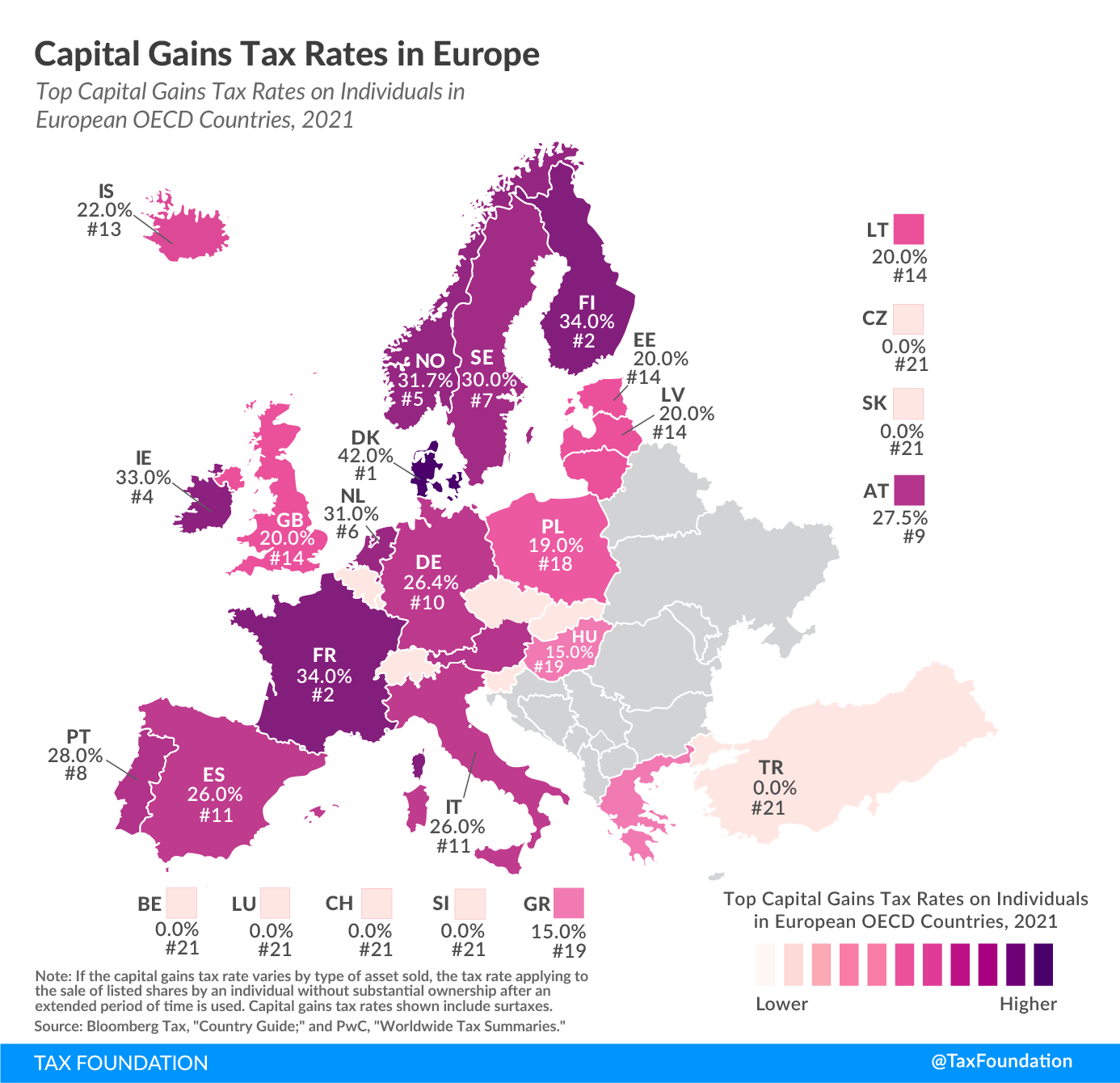

Capital Gains Tax

Since a lot of tax legislatures see Bitcoin as an asset, disposing of an asset is always a capital gain, subject to appropriate tax. In a lot of countries, selling cryptocurrency is taxed the same way selling a house would be taxed. Therefore, a simple Bitcoin uses: selling for fiat currency, swapping for another cryptocurrency, spending it on goods or services, gifting it (in the UK) incur the Capital Gain Tax on the value of your Bitcoin gains. This means you are not taxed for the full value of your Bitcoin but for any profit you’ve made from selling, swapping, or spending it.

Important to notice is the taxation of the profit you’ve made. The cost of the coins plus any fees constitute the cost basis for your Bitcoin capital. Value at disposal minus the coin basis gives a figure, positive or negative. A positive number means you have a profit, which is a capital gain, hence taxable. A negative number is a capital loss. You will want to keep track of those, as they can offset against your gains to reduce the overall tax bill.

How will the tax office know about my Bitcoin?

Due to the nature of Bitcoin, it is not easy for tax offices to keep track of the transactions. But since the legal acts are in place tax offices are pressuring the large crypto exchanges to share customer information (KYC – know your customer regulations).

Are there any crypto tax havens in Europe?

There is no uniform policy for taxing cryptocurrencies. Some nations take a more liberal approach than others. While it may seem that certain countries offer a tax-free stance on Bitcoins, there are usually very specific provisions that vary from state to state.

Belarus

Belarus has decided to exempt individuals and businesses from taxes until 2023. Mining and investing Bitcoin is deemed a personal investment, exempt from both income and capital gain taxes.

Portugal

Portugal has one of the most crypto-friendly tax laws in the world. Proceeds from the trade and sale of Bitcoin and other cryptocurrencies are not considered income. Only the businesses that accept Bitcoin as payment for goods and services are liable to income tax.

Slovenia

For individuals, selling Bitcoin and all the related profits are not considered income. However, the companies involved with mining or any other aspect of Bitcoin trade are subject to taxation. Interesting is that token issuing during the ICO phase is taxed up to 50%. There are still regulative insecurities that local crypto communities are working with the government to smooth out and bring more clarity.

Switzerland

For individuals who qualify, profits made by trading or investing in Bitcoin are tax-exempt capital gains. Only those who trade professionally, be it individuals or businesses are subject to income tax. However, due to regional differences as well as the annual “wealth tax”, the total amount of cryptocurrency owned is added to an individual’s net worth and thus subject to tax.

Germany

Germany’s tax laws are viewing Bitcoin as a private asset. This means that Bitcoin attracts an individual income tax rather than a capital gain tax. Short-term trading, mining, staking are considered income, while still being exempt from taxes if the gains don’t surpass 600 EUR. There is no tax on Bitcoin sales after a holding period of one year. Therefore, Germany supports tax-free profits from cryptocurrencies only if they are used for long-term financial investment.

UK

United Kingdom’s laws see Bitcoin as property – a capital asset. However, the taxation is depending on specific transactions you are making with your cryptocurrency. Basically, if you are earning cryptocurrency, it’s seen as income. If you are selling or swapping it, then it’s taxed as a capital gain. Again, you are not required to pay tax on the entire proceeds, only on the profit gained.

Capital gains tax rates in the UK are 10% for those with regular income up to 50,270 GBP and 20% for those with regular income above. There is a personal income tax allowance of 12,570 GPB. Basically, your first income up to the designated amount is tax-free. The trading and property allowance is 1000 GBP (that’s how your crypto trading can be tax-free for the first 1000 GBP earned). Another important thing to have in mind is UK’s capital gains tax-free allowance. Namely, you pay taxes for capital gains larger than 12,300 GBP. You can still use capital losses to stay within this allowance.

UK laws consider getting paid in Bitcoin, airdrops (free tokens), mining, and staking rewards to be income. All of DeFi rewards are considered income as well, so yield farming, liquidity pool bounty, staking rewards are considered income. Fun fact. If you are doing speculative day trading of cryptocurrencies, under UK laws it is considered gambling, and therefore no tax applied.

FAQ

Q: Bitcoin is legal in all of the EU and UK?

A: Yes. Bitcoin is legal. It is legal to buy it, sell it, own it, or mine it.

Q: So, Bitcoins are taxable?

A: Yes. Buying or holding Bitcoin is not taxable. Depending on the country you are paying your taxes in, selling Bitcoin creates a tax event, and profits above a certain limit are taxable.

Q: How is the value of Bitcoin calculated for the purpose of determining gains or losses.

A: This is why keeping records is very important. If you sell Bitcoin, gains and losses are calculated by comparing the price value at the moment of purchase vs price at the moment of disposal.

Crypto Ping Pong Digest

Trash style news. You will definitely like