Table of Contents

Decentralized Finance (DeFi)

There are numerous misconceptions about the very nature of blockchain technology. One of the most prominent ones is that blockchain is value-neutral. However, exactly in the case of decentralized finance (DeFi), we can see an entire movement (if not ideology) aimed mostly at giving the people financial freedom from traditional, centralized finance.

DeFi is a paragon of the blockchain’s real use case. Besides being a well-designed attempt at solving the problems of traditional finance such as centralization or ‘built-in’, pre-designed inequality between service providers and users, it tries to overcome issues of lacking personal autonomy and ownership over one’s personal finances, mainly by providing disintermediation between the people.

DeFi consists of various sets of financial services, including decentralized exchanges (DEXs), yield farming or liquidity provision platforms, decentralized autonomous organizations (DAOs), borrowing/lending platforms, payment gateways, and many others.

DeFi 2.0 Evolution: What’s New?

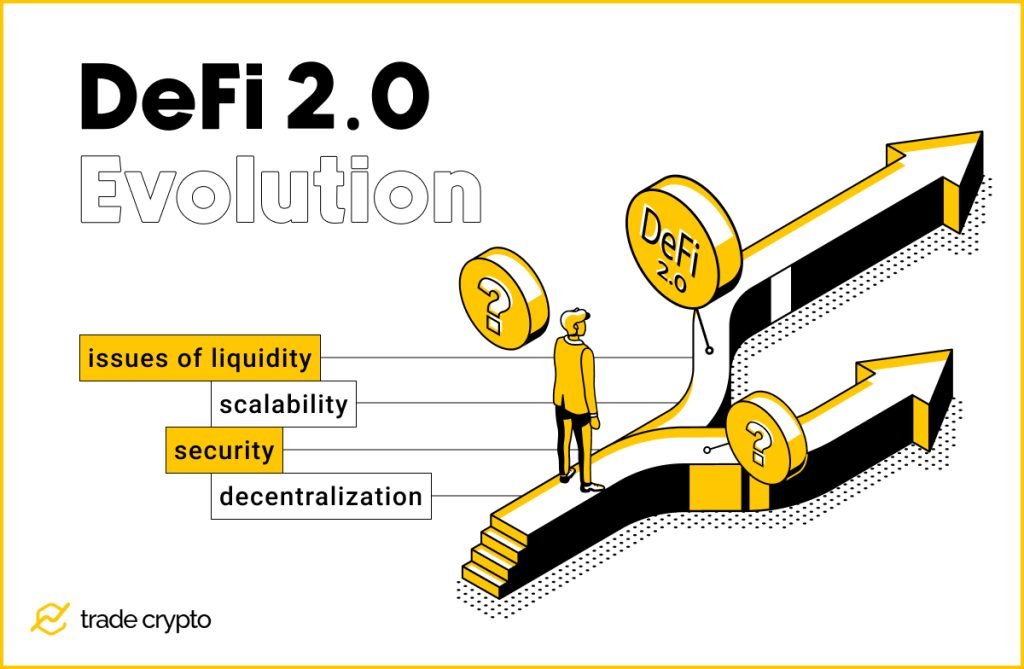

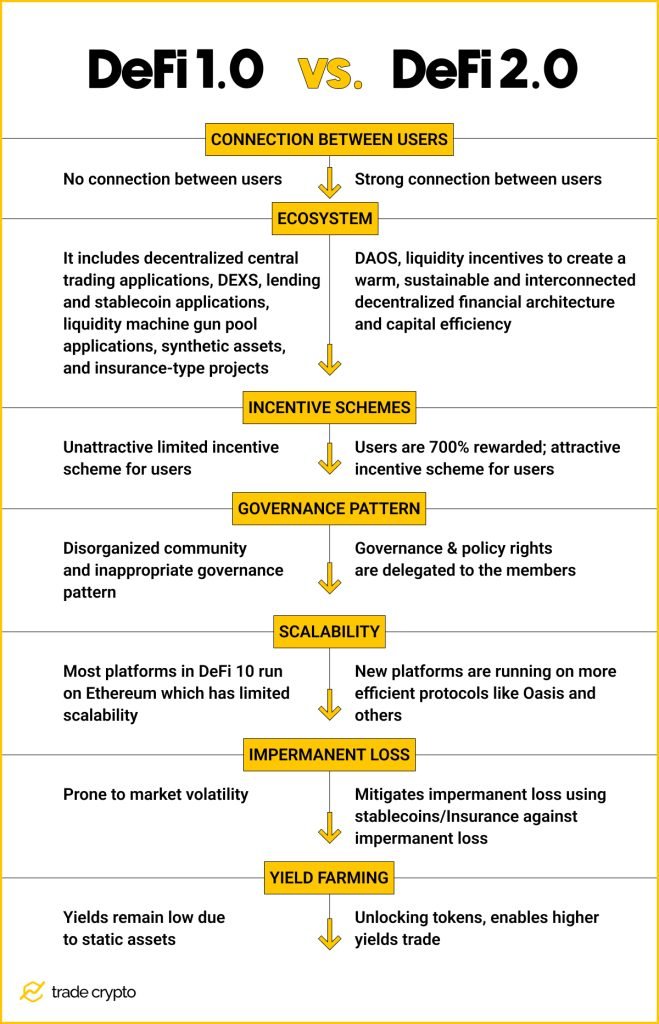

The mentioned features were brought already by the first wave of decentralized finance, called Defi 1.0. But, DeFi 1.0 ecosystem had several limitations that had to be addressed. The rapid evolution of inherently somewhat flawed DeFi 1.0 lead to the creation of DeFi 2.0, with many improvements regarding the issues of liquidity, scalability, security, and decentralization.

Early DeFi stakeholders (e.g. Uniswap, Aave, Bancor, MakerDAO, Compound) built the crucial foundation for creating the entire landscape of the DeFi economy.

By providing the possibility to swap tokens without giving up custody, decentralized lending, and borrowing platform, and a decentralized stablecoin as a buffer against the volatility of cryptocurrencies, DeFi 1.0 allowed users to gain access to dependable exchanges, frictionless lending/borrowing, and pegged currencies – the three key crypto-economy primitives that changed the world of global finance.

DeFi 2.0 has had to solve several fundamental problems inherent to the older decentralized finance model. Not only does it fix its existing flaws, but it also leverages strengths and takes it to another level.

Inclusion and Usability Issues

Older DeFi 2.0 platforms were not particularly user-friendly. As their user interfaces and UX were complex and hard to navigate, they were used mostly by the already experienced users, leaving the newbies out. By improving UX and UI, new parts of the DeFi ecosystem have provided digital inclusion, ultimately needed for DeFi 2.0 to go mainstream.

The inclusion and user experience were also hindered by high fees and long wait times. As the majority of DeFi platforms are based on the Ethereum platform, transactions often get stuck and heavily delayed because of a large number of active users, causing fees to skyrocket. That has been another case of financial exclusion because users with less than a few thousand dollars have not been able to make any substantial profit.

Ethereum Platform Scalability Issue

One of the key components of innovation was the improvement of scalability. Decentralized financial services such as Solana, Binance Smart Chain, or Polygon introduced new solutions. Still, there is a lot more to be covered, which may be the case for a future DeFi 3.0 furtherly addressing high gas prices and Ethereum network transaction traffic jams.

Yield Farming

To attract new users – token holders and their fresh capital, DeFi 2.0 markets have to provide them with the option of earning yields.

Yield farming has become a general term for all activities in DeFi which generate a return (yield) on a type of digital asset collateral, usually calculated in Annual Percentage Yield (APY). Yield farming can be loosely synonymized with interest or dividend.

Lending

A standard way to collect yield is by users providing loans in return for interest payments. Self-repaying loans offer a significantly higher degree of certainty for everyone as the future yields on assets deposited by the lender are used for paying off debt automatically.

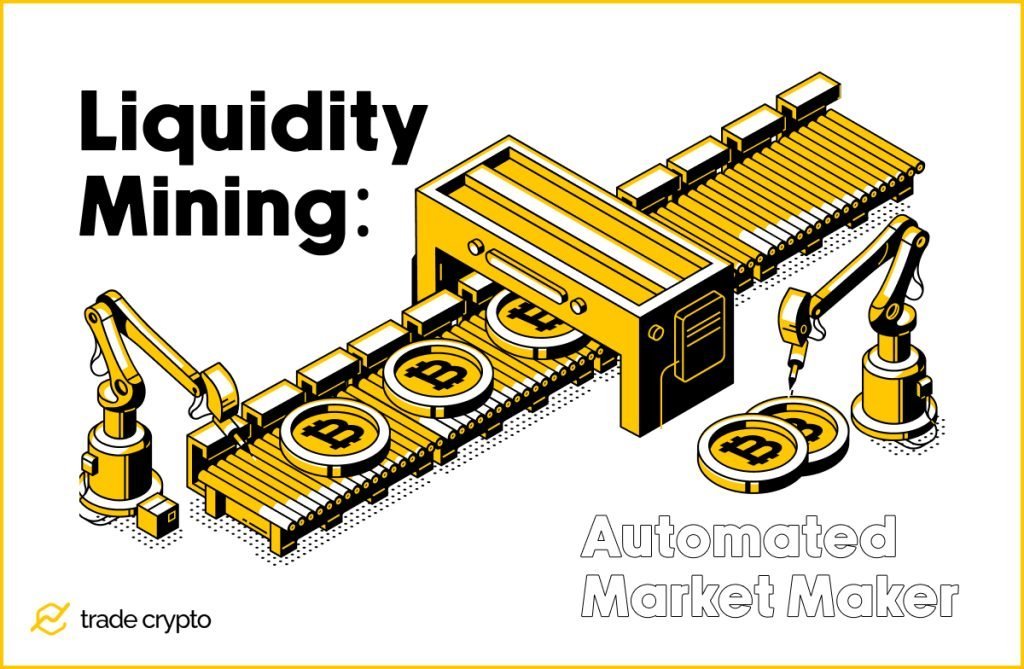

Liquidity Mining

DeFi 2.0 liquidity pools offer higher rewards for earning more liquidity than their predecessors. The platforms acquire assets that manage their liquidity and in turn, provide benefits like token trading, collateralized crediting, or rewards for users who bootstrap liquidity by staking assets.

Automated Market Maker (AMMs) is an underlying protocol used by decentralized exchanges that allow digital assets to be traded permissionless and automatically by using liquidity pools instead of a traditional market of buyers and sellers. They allow every person with sufficient funds to provide liquidity for a token pair.

Rather than provisioning liquidity themselves, liquidity mining providers may secure the liquidity from other users. But, users are hesitant about securing liquidity for a new coin because it makes them exposed to the risk of a loss.

In case there is not enough liquidity generated, it can be boosted by liquidity providers issuing liquidity mining provider (LP) tokens. This specific version of yield farming is quite straightforward: users offer liquidity for an exchange pair via an AMM protocol, receive LP tokens in exchange, and then stake LP tokens for returns in the liquidity providers’ native token.

By offering high returns and minimalizing slippage for new users, the creation of a liquidity pool and LP tokens has become a norm for bootstrapping funding of DeFi 2.0 projects.

Centralization: DAOs

The aspect of decentralization is an important part of DeFi protocols. Decentralized Autonomous Organizations (DAOs) are constructed by rules encoded as a computer program (smart contract) that is transparent, controlled by the organization’s members, and not managed by a central government. Being member-owned communities without centralized leadership, DAO is a preferred way of governance in the DeFi 2.0 environment.

DeFi 2.0 vs. DeFi 1.0 Infographic

DeFi 2.0 Real Use for Investors

Defi projects have additionally democratized investing by lowering the threshold for entering the arena of trading crypto-assets and devising financial primitives that can overcome the limits inherent to traditional financial services. Pushing decentralized finance forward has increased the global size of the DeFi user base and those defi users are now creators of a new, disruptive financial order.

Buying DeFi 2.0 Platform’s Native Tokens

The simplest way to invest in DeFi 2.0 is to use a DeFi 2.0 project’s platform to buy and trade its native token. If the project succeeds, that will subsequently maximize profit made by the increasing value of token investment (except if it is a stablecoin). This is even more straightforward than the yield farming options we mentioned in the previous section.

Cross-chain Trading

Deployment of smart contracts and liquidity pools can interconnect different blockchains and DeFi platforms. By surpassing the limits of an individual DeFi 2.0 platform, users can gain access and trade assets on multiple DEXs.

Self-repaying Loans

Many DeFi 2.0 projects allow using their LP tokens as collateral for a loan. While earning interest on a collateral token, users can benefit additionally from taking a loan (and perhaps earning liquidity mining rewards simultaneously).

Staking

Users can decide to become validators for a proof-of-stake blockchain and earn block rewards by locking that chain’s validator currency.

Smart Contract Insurance

The risk in DeFi 2.0 projects is mitigated by availing of insurance on specific smart contracts. If the user has staked liquidity provider tokens on smart contracts, then there remains a chance of losing deposits. This is solved by the insurance gotten for a fee.

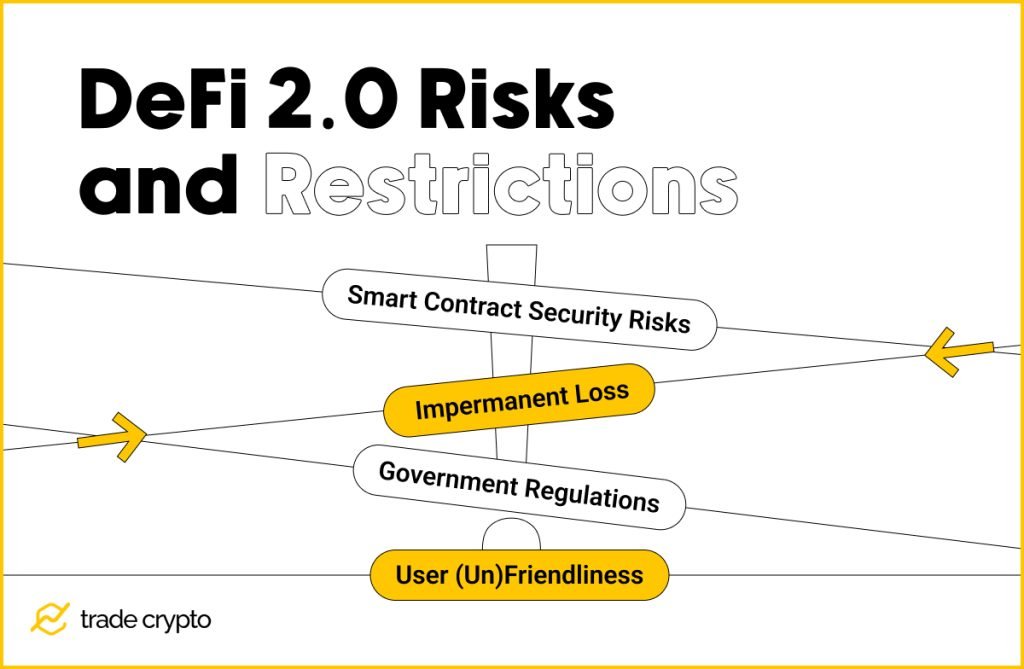

DeFi 2.0 Risks and Restrictions

Smart Contract Security Risks

Every smart contract may have backdoors and other security issues. Although thorough research and prior investigation should be performed before investing, every investment comes with a certain risk level. Security audits of smart contracts can minimize risks, but cannot eliminate them.

Impermanent Loss (IL)

Impermanent loss is a situation where the value of the withdrawal is lower than the value of the deposit. This loss is labeled impermanent because no loss will happen if the cryptocurrency can return to the initial price. Insurance offered by the defi 2.0 platform can alleviate the risk of loss, but in cases of severe market disruption, it may not be enough.

Government Regulations

National governments across the globe constantly impose new regulations regarding crypto markets. Although they may be unfavorable – even hostile – towards them, regulations bring an additional layer of safety for crypto investors.

User (Un)Friendliness

DeFi 2.0 platforms have traveled a long way from older 1.0 defi protocols in terms of user experience. However, the defi 2.0 environment is still a bit rough for an inexperienced user.

DeFi 2.0 List of Projects

Some of the most popular DeFi 2.0 projects are presented below (for a detailed review of them, click here):

Wonderland ($TIME)

The Wonderland project started as a decentralized autonomous organization (DAO) but later evolved into a crypto venture capital fund. The Wonderland team would identify new crypto projects, invest in them, and in return receive the respective projects’ native coins. Some of those coins would be given as a bonus to the investors through an airdrop, but none of them ever happened.

When the situation in crypto markets started to worsen in Q4 2021, Wonderland’s currency (wMEMO) started to plummet and the team decided to institute buybacks – a measure to prevent their coin from falling under a specified price. The team used treasury funds to buy tokens from the open market and push the price up.

Several large investors allegedly colluded on a scheme to lower the price, and cause cascading liquidations. These liquidations would cause the price to fall drastically. They would then buy back in at the lower prices and wait for the buybacks to bring up the price again in an arbitrage strategy. The result: key people bailed out and the project’s native coin has lost over 99% of its value from the ATH level, leaving the investors high and dry.

Abracadabra ($MIM)

Is there something like magic internet money? The creators of Abracadabra believed so when they started their defi 2.0 platform. They were the first ones to introduce the concept of leveraged yield farming.

When you deposit your assets (coins) into a standard yield farm, you receive an interest-bearing token equivalent. These tokens have their own value and can be exchanged for other crypto assets – that is the interest paid to the investor.

Abracadabra uses these tokens as collateral to take out loans, as they are considered cash equivalents. Because they are stablecoins, the cost of taking out the loan is 0.8% and users can take out up to 90% of the value these coins represent (the stablecoin has to lose 10% of its value for you to be liquidated).

A practical example:

- The investor deposits 1,000 USDC into a Yearn-USDC Vault, which generates a hypothetical 4.5% annual percentage yield (APY). After depositing USDC, the user receives yvUSDC, interest-bearing tokens which represent the initial investment plus accrued interest.

- The user then deposits their yvUSDC tokens as collateral to take out a loan on the Abracadabra platform. For the user’s yvUSDC tokens, the loan costs 0.8% and the user can borrow up to 90% of the collateral value.

- The user is earning 2.5% on the USDC they deposited and has taken out a loan on Abracadabra that costs them 0.8% a year while holding $MIM tokens representing 90% of their USDC value. In a word, the investor has $900 worth of liquid $MIM and still earning a net 3.7% APY on their original deposit (4.5% APY minus the 0.8% interest charged for the loan on Abracadabra).

The things get even sweeter – you can take that liquid money (the 90% of your original stablecoin stack) and use them to make more money by repeating the loop of the same process (deposit into yield farm – take out a loan – deposit into yield farm). Depending on how many times the loop is performed (the system allows up to 10x), a $100k investment can get yield farming returns as if it were $500k, or $1m, minus loan interest fees.

And that is exactly the defi 2.0 concept of leveraged yield farming (nice video tutorial can be found here).

Curve ($CRV) and Convex ($CVX)

To put it simple: Curve is the DAO, exchange, LP, stablecoin and more, on which the yield farming platform Convex is built. Curve finance platform

Curve is an important defi protocol as it operates as the base layer for many other protocols in crypto world. It is the best place to swap tokens that have a similar price, such as from one stablecoin to another. Its math so so good that guarantees lowest fees and very low risk of slippage.

In fact, it is SO good that its data have been intensively used by Chainlink – the topmost valuable blockchain oracle. Paradoxically, when you ask Chainlink about a coin’s price, the silent entity that provides the exact answer is – Curve.

CRV is Curve finance governance token. Holders can lock up CRV tokens and in return, they get veCRV tokens in exchange. These ‘validators’ can expect a boost in yield farming rewards against the deposited means of liquidity (assets), and they receive transaction fees for every trade made on Curve. But these crypto holders must be patient – CRV has to be locked up for years at a time – the longer it is locked up, the more powerful the above three benefits are.

Most people do not have enough CRVs to lock up to achieve the maximum benefits, nor are they willing to do that, and this is the Convex use case.

The Convex protocol takes CRV and locks it all up as one big entity. Currently, the Convex protocol is the largest holder of locked-up CRV (over 50%). As a singular entity, it experiences the maximum benefits of locked-up CRV while allowing its users to experience these benefits freely.

TradeCrypto DeFi 2.0 Verdict and Prediction

The nascent world of blockchain initially attracted various visionaries, cyber-libertarians, digital anarchists and other people existing on the fringes of tech-laden societies, seeking for more financial justice and democracy by disintermediation and disempowering the stakeholders of traditional finance

However, as cryptocurrencies appeared, they instigated the desire of an ordinary person to get rich fast. But, they were not designed for that purpose nor they are able to do that. There is no easy money, especially these days in crypto world. DeFi evolution and especially defi 2.0 2.0 novelties have provided a huge step forward in crypto finance.

Although a high degree of caution regarding the defi space’s continuing progress is warranted, we believe the next upswing of the ecosystem will bring about a new, improved DeFi 3.0 environment.

Crypto Ping Pong Digest

Trash style news. You will definitely like